If you have compared two shopping centers on visit numbers and one looked twice as busy as the other, the honest answer is that you may have been comparing two different animals. A neighborhood grocery center and a superregional mall both count "visits," but a household hits the first one weekly for twenty minutes and the second one a few times a year for three hours. The raw number tells you almost nothing until you know which format you are looking at.

Shopping centers sort into recognized types, and the type sets the expectation for how big the property is, what anchors it, how far people travel to reach it, and how footfall behaves once they arrive. This is a reference to that typology: the standard classes, what separates them, and why the classification is the first thing you fix before you benchmark anything.

The classification is not academic tidiness. It is the frame every investor, valuer, and leasing team uses to decide what a center should look like, who should anchor it, and what a healthy footfall figure would even be. A supermarket that would anchor a community center perfectly well would look undersized fronting a superregional mall, and a full-line department store that suits a regional center would swallow a neighborhood center whole. Get the format wrong in your head and every downstream judgment, rent expectations, tenant mix, target dwell, drifts off with it.

What is the difference between a regional and a community shopping center?

The two differ in size, anchor type, and how far shoppers travel. A community center is mid-size, anchored by a supermarket, a discount department store, or a drugstore, and serves a local trade area for routine shopping. A regional center is much larger, anchored by one or more full-line department stores or large-format retailers, and pulls shoppers from a wider area for comparison and discretionary shopping. The bigger draw and the longer trip mean regional centers tend to see higher dwell per visit but lower visit frequency than a community center. Put simply: people go to a community center often and briefly, and to a regional center rarely and at length.

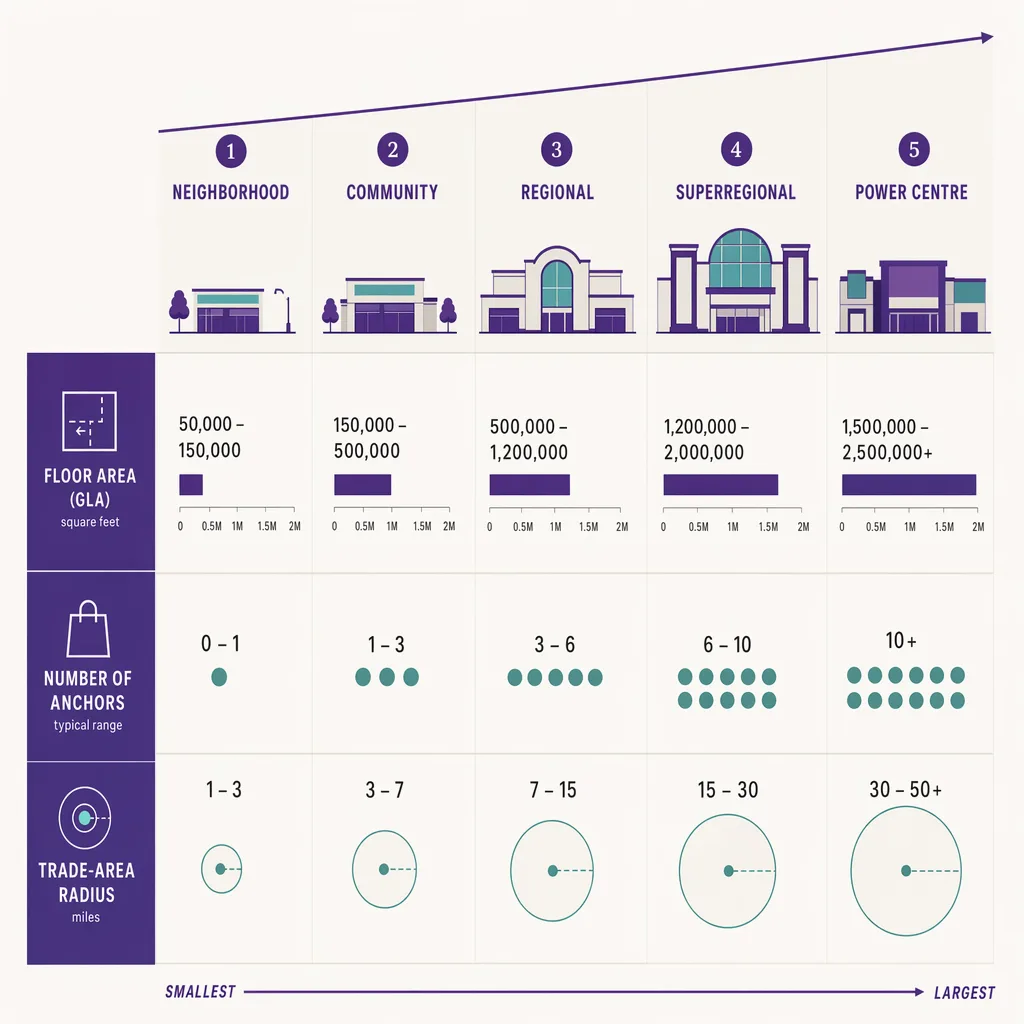

The standard classification, format by format

The retail industry classifies centers along a consistent spine: gross leasable area, the kind of anchor, and the size of the trade area the center draws from. The exact size bands vary between classification schemes and between countries, so treat the figures below as directional rather than as fixed thresholds. What stays stable across schemes is the ordering and the role of each format.

Neighborhood center

The smallest of the convenience formats. A neighborhood center is anchored by a supermarket, sometimes with a drugstore alongside, and exists to serve the daily and weekly needs of the households immediately around it. The trade area is small, often a short drive or walk. Tenants are convenience-led: a pharmacy, a bakery, a dry cleaner, a quick-service food unit. Footfall is high-frequency and short-dwell, driven by the grocer's repeat pull.

Community center

A step up in size and range. A community center adds a wider general-merchandise offer to the convenience base, anchored by a supermarket plus a discount department store, a large drugstore, an off-price apparel store, or a home-goods retailer. The trade area is larger than a neighborhood center's, and the tenant mix reaches beyond daily needs into soft goods and services. Footfall is still frequency-led but the visit is longer than at a pure grocery center, because there is more to browse.

Regional center

The classic enclosed mall. A regional center is anchored by one or more full-line department stores or large-format retailers and offers a deep, comparison-shopping tenant mix across apparel, footwear, electronics, and services. The trade area is regional: shoppers travel a meaningful distance and treat the trip as an outing rather than an errand. That produces the pattern noted above, lower frequency and much higher dwell, with weekend and holiday peaks that dwarf a community center's flatter weekly rhythm.

Superregional center

A regional center scaled up. A superregional has more gross leasable area, more anchors, and a still-wider trade area, often drawing from an entire metropolitan region and sometimes pulling day-trip and tourist visits. The dwell-heavy, event-style visit pattern of a regional center is even more pronounced here, and the center often layers in dining, cinema, and entertainment to extend the length of stay.

Power center

A different shape entirely. A power center is dominated by several big-box anchors, category-leading stores in home improvement, electronics, warehouse-club, off-price apparel, or pet, with relatively little inline space between them. Shoppers often drive to one specific big box, park close to it, buy, and leave, so the format can produce high entry counts with lower cross-shopping between stores than an enclosed mall. Some of that draw comes from stores the center does not even lease, a pattern worth understanding on its own.

Lifestyle center

An open-air format built around dining, services, and higher-end specialty retail rather than a single dominant anchor. Lifestyle centers lean on dwell and atmosphere: the design encourages lingering, eating, and browsing across a walkable layout, so the value sits in time spent rather than in a department-store draw. The anchor role is often played by a cinema, a food hall, or a cluster of destination restaurants instead of a traditional big-box tenant.

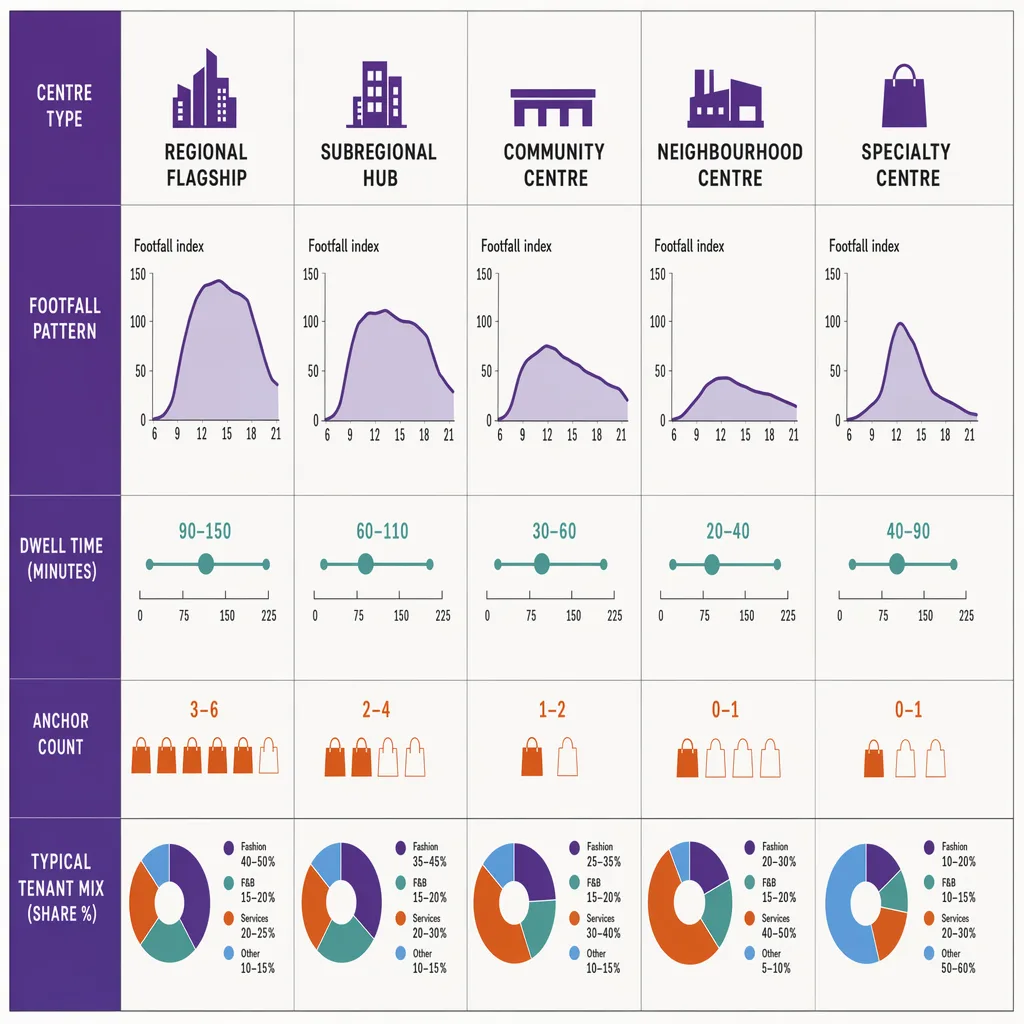

How footfall behaves by center type

The typology matters because footfall reads differently in each box, and the two dimensions that separate the formats are visit frequency and dwell time.

At the convenience end, neighborhood and community centers, the grocer or discount anchor drives frequent, short visits. A household may pass through several times a week, so the center accumulates a large visit count from a modest catchment, but each individual visit is brief and purposeful. That frequency is the format's strength: it is why grocery-anchored properties are prized for steady, defensive cash flow.

At the destination end, regional and superregional centers, the pattern inverts. Visits are less frequent but far longer, clustered into weekends, evenings, and holiday periods, and the shopper is in a browsing-and-comparison mode that a convenience trip never enters. Dwell becomes the metric that actually describes the center, which is why dwell time benchmarks are far more meaningful for a mall than for a grocery center.

Power centers sit apart again: high, spiky entry counts tied to specific big-box destinations, often with less movement between stores than the enclosed formats. A shopper drives to the home-improvement store for a specific project, buys, and leaves, so the center can post a strong door count while the inline tenants between the big boxes see far less of that traffic than a mall corridor would capture. Lifestyle centers behave more like regional centers on dwell but without the single-anchor spike, since the draw is distributed across dining and specialty rather than concentrated in a department store, and the visit is often driven by a meal or an evening out rather than a shopping list.

The practical consequence is that the same word, "busy," means four different things across these formats. A busy neighborhood center is one that a large local population passes through repeatedly. A busy regional mall is one where a smaller number of shoppers each stay for hours. A busy power center is one where specific big boxes pull hard on specific days. A busy lifestyle center is one where people linger over food and atmosphere. Any footfall figure has to be read against the format's own definition of busy, not a single cross-format yardstick.

Anchor type by center type

The anchor is the clearest tell of the format, and it is where this typology connects to the wider anchor discussion. Each format leans on a characteristic anchor: a supermarket at the neighborhood and community end, a full-line department store at the regional and superregional end, and category-killing big boxes in a power center. As full-line department stores have retreated over the past several years, the regional format has felt the most pressure, which is exactly why so much redevelopment activity targets that box.

If you are new to the anchor concept itself, start with the fundamentals in what an anchor tenant is, and see the shift away from department-store anchors for why the regional mall is the format under the most strain. The department-store retreat is the single biggest reason the regional and superregional formats have had to change: when the box that defined the format empties, the center either backfills it, subdivides it, or converts it, and each of those moves nudges the property toward a different class than the one it started as. A regional mall that fills two dark department stores with a gym, a food hall, and a medical suite is no longer a pure comparison-shopping center, and its footfall shifts toward the frequent, service-led pattern of a lower tier.

The relationship also runs the other way. The convenience formats have held up precisely because their anchor, the grocer, sells things people buy every week in any economy. That defensive, high-frequency profile is what makes grocery-anchored centers attractive to investors who want steady cash flow rather than discretionary upside, and it is why capital has flowed toward the community and neighborhood end while the regional end has had to reinvent itself. The anchor is not just a tenant on the rent roll; it is the thing that decides which of these six boxes a property actually lives in.

Why the classification comes first, before any benchmark

Here is the practical payoff, and the reason this typology is not just academic. You cannot compare a community center to a superregional on raw visits and learn anything useful. The community center will often show more total visits, because frequency stacks up, while the superregional shows a fraction of the count at many times the dwell and spend per visit. Reading the first as "busier" and therefore "better performing" is a category error.

The same trap catches format comparisons on vacancy and dwell. An open-air power center and an enclosed regional mall do not fail the same way, and their footfall does not recover the same way, which is why outlet and mall formats reward different measurement, and why vacancy and footfall interact differently by format. Fix the format first. Then benchmark like against like: community against community, regional against regional, power against power. Only inside a format does a footfall comparison carry a clean signal.

How you would benchmark footfall by center type

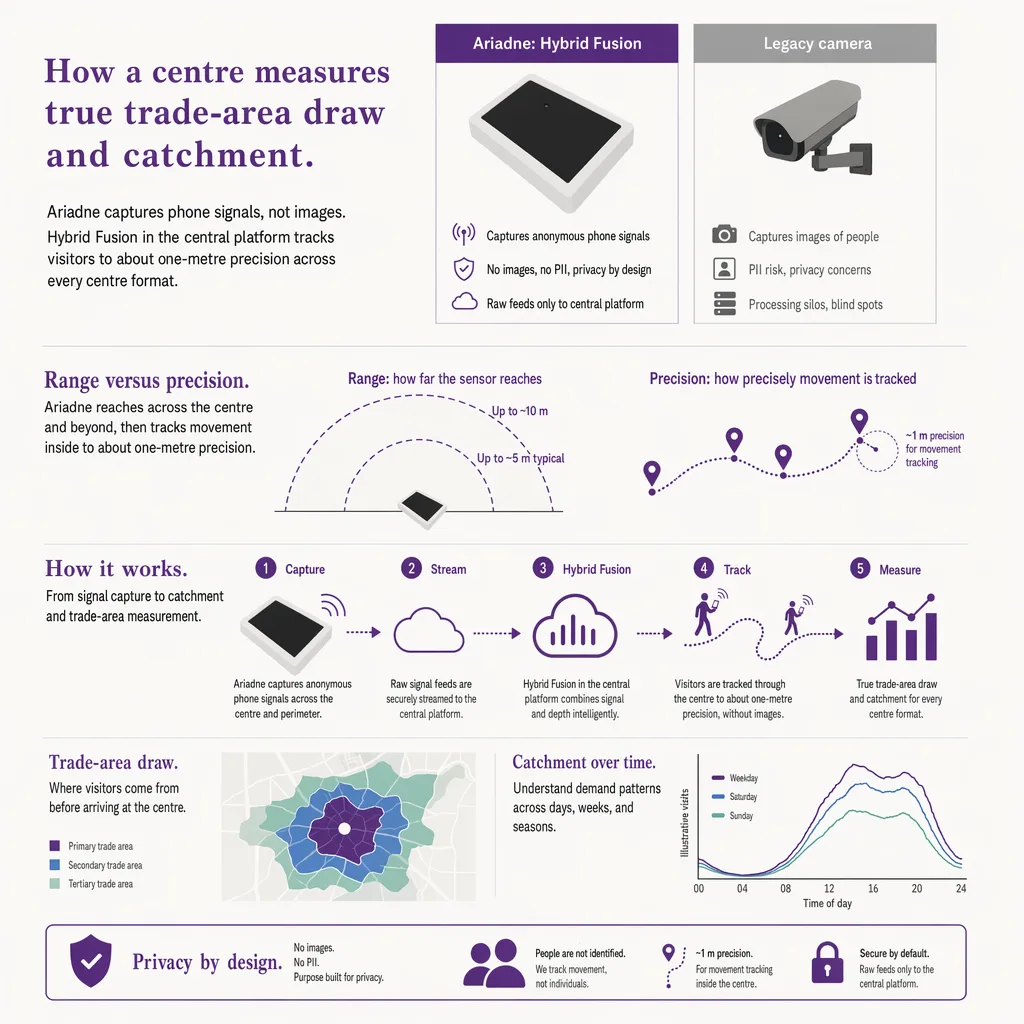

Ariadne measures this with Hybrid Fusion, its patented camera-free method. Time-of-Flight depth sensing counts every visitor at the entrances, capturing geometry rather than images, while patented phone signal sensing follows movement through the interior, detecting the signals a phone emits even in airplane mode. The sensor streams both feeds to Ariadne, where Hybrid Fusion combines them into one trajectory per visit and computes counts, dwell, and paths. The streams carry no identifier: no MAC address, no device ID, no biometric data, and no camera is involved. Identifiers are stored only when a visitor explicitly opts in, which keeps the method GDPR-friendly and outside biometric territory.

Because the method produces both the entry count and the dwell per visit, it gives you the two numbers the typology says actually separate the formats, rather than a single "visits" figure that flattens a community center and a superregional into the same misleading line. A landlord comparing properties across a portfolio can then hold format constant and read the numbers that mean the same thing within a class. That reference frame is the point of shopping center analytics: a count is only interpretable once you know which format produced it.

FAQ

What are the main types of shopping centers?

The standard classes are neighborhood, community, regional, superregional, power, and lifestyle centers. They are separated by gross leasable area, the type of anchor, and the size of the trade area the center draws shoppers from.

Is a community center bigger than a neighborhood center?

Yes. A neighborhood center is the smallest convenience format, usually anchored by a single supermarket. A community center is larger, adds a wider general-merchandise offer, and typically pairs the grocery anchor with a discount department store, drugstore, or off-price retailer.

What is the difference between a regional and a superregional mall?

Size and reach. A superregional center has more gross leasable area, more anchors, and a wider trade area than a regional center, often drawing from an entire metropolitan region and layering in more dining and entertainment to extend the visit.

What is a power center?

A power center is dominated by several big-box anchors with little inline retail between them. Shoppers tend to drive to one specific store, buy, and leave, so the format produces high entry counts with less cross-shopping than an enclosed mall.

Why does the center type matter for footfall benchmarking?

Because footfall behaves differently by format. Convenience centers see frequent, short visits, while regional and superregional centers see infrequent, long ones. Comparing raw visits across formats is misleading, so you benchmark within a format, not across formats.

What is a lifestyle center?

An open-air format built around dining, services, and higher-end specialty retail rather than a single dominant anchor. The draw is atmosphere and dwell rather than a department store, so the anchor role is often played by a cinema, a food hall, or a cluster of destination restaurants, and the value shows up in time spent rather than in a big-box entry spike.

Are these shopping center classifications the same in every country?

The names and the ordering are broadly consistent, but the exact size bands differ between classification schemes and between markets. Treat the gross-leasable-area figures as directional. What stays stable everywhere is the role of each format: convenience at the small end, comparison shopping in the middle, big-box destinations in the power format.

---