Search for "anchor tenant examples" and most results stop at the definition, then hand you one or two obvious names and move on. That is not what the query wants. If you are looking for examples, you want a proper list: which kinds of stores anchor which kinds of centers, and why each one earns the role. The specific brands shift by country and change as retail changes, but the categories are stable, and knowing them tells you more than any single logo does.

This is a structured catalogue of anchor tenants by center format. It covers the classic department-store and supermarket anchors, the big-box and warehouse-club anchors of a power center, and the newer draws (cinema, gym, food hall) filling space the old anchors left behind. For the underlying definition and the broader economics, see what an anchor tenant is; this post assumes you already have the concept and want the examples.

What are some examples of anchor tenants?

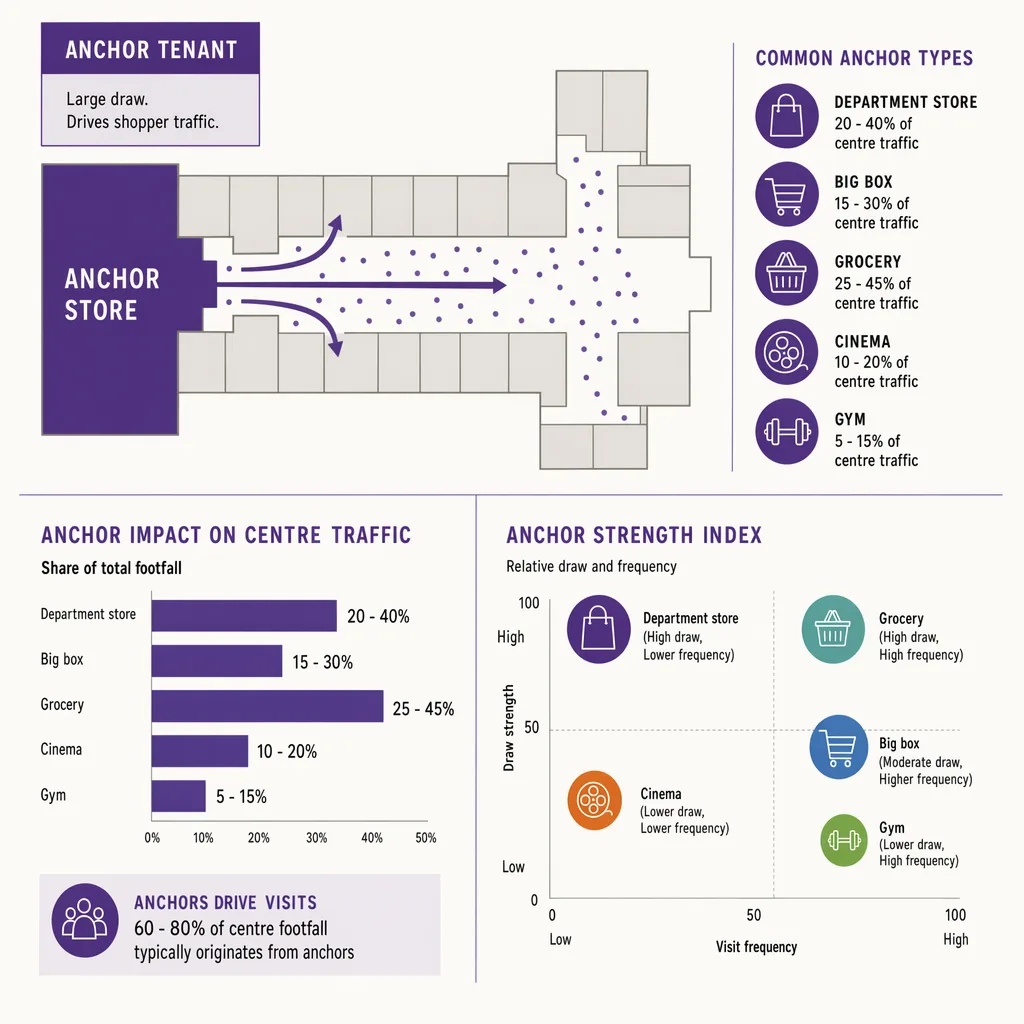

An anchor tenant is the large, high-traffic store a shopping center leases to pull shoppers in, who then spend at the smaller inline shops. Common examples by format: department stores and large-format apparel in regional malls, a supermarket or hypermarket in a community or grocery-anchored center, a home-improvement or warehouse-club store in a power center, and increasingly a cinema, gym, or food hall where a department store used to sit. The specific brands differ by country, but the role is the same: draw the crowd the rest of the center lives on.

The rest of this post walks each format in turn, because the reason a store anchors a regional mall is not the reason a store anchors a strip center, and mixing them up is where a lot of casual explanations go wrong.

Department store and apparel anchors (regional malls)

The department store is the anchor most people picture, and for good reason: it defined the enclosed regional mall. In the United States, the names that carried that role for decades are the ones now most associated with its decline, including Sears, JCPenney, and Macy's, all of which have closed large numbers of full-line stores across the 2020 to 2025 period. Their footprints were built precisely to anchor: a store large enough that a shopper would make a dedicated trip, positioned at the ends of the mall so foot traffic between anchors dragged past every inline shop in between.

Large-format apparel and fast-fashion retailers have taken on some of that pulling power as full-line department stores retreat. A big apparel format that draws its own dedicated visits can hold an end of a mall the way a department store once did, though usually in a smaller box. The role is identical: be the reason the shopper drove to this center rather than shopping online.

Outside the United States, the same category filled the role under different names. Britain leaned on its own department-store tradition, and the closures there followed a similar arc across the same 2020 to 2025 window, most visibly with the collapse of the Debenhams chain, whose stores had anchored high streets and centers for generations. The pattern travels: a large, range-heavy store that once defined the trip loses its pull, and the space it held becomes the hardest problem a landlord faces. The country changes, the mechanics do not.

What matters for anyone studying examples is not the individual name but the function. A department-store anchor works because it combines scale, a wide product range, and a brand strong enough to be the trip's purpose. When you evaluate whether a given store is a "real" anchor, that is the test: is it the reason people came, or is it living on traffic someone else brought. Two stores of identical size can play opposite roles. One is the destination that fills the parking lot; the other is a large tenant that happens to sit inside a center other stores fill. Only the first is genuinely an anchor, and the difference is invisible on a floor plan. It shows up only in where the traffic originates.

Grocery and hypermarket anchors (community centers)

Step down from the regional mall to the community or neighborhood center and the anchor changes character entirely. Here the draw is a supermarket or a hypermarket, and the traffic it pulls behaves very differently from a department store's. Grocery visits are frequent and necessity-led: a household shops for food weekly or more often, which means the anchor produces steady, repeat footfall rather than the occasional discretionary trip a mall depends on.

That is why grocery-anchored centers are treated as a defensive property type. People keep buying food in a downturn, so the anchor keeps pulling traffic when a discretionary regional mall would soften. The inline mix around a grocer reflects the repeat-visit pattern: pharmacy, dry cleaner, quick-service food, a bank branch, the kinds of errands a shopper folds into the same trip.

In Europe, the hypermarket plays a larger anchoring role than in North America, often as the dominant tenant of a suburban center rather than one anchor among several. The category is the constant: a food retailer big enough to be the routine destination for a local trade area.

The difference in visit rhythm has real consequences for how these anchors are leased and valued. A department-store anchor is judged partly on the discretionary spend it draws on a weekend; a grocery anchor is judged on how reliably it brings the same households back through the week. That reliability is why grocery-anchored centers changed hands at firmer valuations than discretionary malls through the disruption of the early 2020s, a preference well documented across commercial real-estate commentary of the period. For the landlord, a grocery anchor is closer to a utility than a fashion statement, and the inline tenants that do best around it are the ones that suit an errand rather than a browse.

Big-box, warehouse-club, and home-improvement anchors (power centers)

The power center is a different animal again. Instead of one or two big anchors surrounded by many small inline shops, a power center is built almost entirely from large-format "category killer" stores, each a destination in its own right. The anchors here are warehouse clubs, home-improvement retailers, large electronics or home-goods formats, and discount department stores.

The economics differ from an enclosed mall. There is little true inline space to protect, so the center depends less on internal foot traffic flowing between anchors and more on each big box drawing its own dedicated visits from the parking lot. A home-improvement retailer does not need the shopper to wander past a jeweler on the way in; the trip is planned and specific.

Warehouse clubs sit at the strong end of this category because they combine scale with a membership model that guarantees repeat visits. A member who pays an annual fee has a reason to keep coming back, so the club produces a predictable base of dedicated trips rather than depending on passing traffic. Home-improvement retailers earn their anchor status differently: their trips are project-driven and often high-value, and a shopper mid-renovation returns repeatedly over weeks. Both are destinations in the truest sense, which is exactly why they can hold a power center that has almost no traditional inline space to protect.

This is also the format where the line between a leased anchor and a nearby draw gets blurry, which is worth flagging: a big-box store next door that a center does not actually lease can still pull the same crowd. That borrowed-traffic case is a distinct concept with its own risks, covered in the shadow-anchor discussion elsewhere in this cluster.

The new anchors: cinema, gym, food hall, and mixed-use

The most interesting examples in 2026 are the ones filling space the department store vacated. When a full-line anchor closes, a landlord rarely finds another department store to take 100,000-plus square feet. Instead the box gets repurposed, and the replacements are experiential rather than transactional.

Cinemas, fitness clubs, and food halls have become anchors in their own right because they do something a shopper cannot do online: they sell time spent in the building. Dining, in particular, has moved from an afterthought to a primary draw. A well-run food hall pulls dedicated evening and weekend visits and holds people in the center for longer than a shopping trip would. That shift is significant enough to treat as its own topic; see food and dining as the new anchor for how food-and-beverage now anchors centers that once relied on retail alone.

These experiential anchors change the traffic pattern as much as they fill the space. A department store pulled its heaviest crowds on weekend afternoons; a cinema and a food hall shift the peak into the evening and stretch the visit past the point where a shopper would otherwise have left. A gym adds something rarer still, a weekday-morning and early-evening flow on a fixed weekly rhythm, which smooths out the traffic curve a purely retail center would leave lumpy. For a landlord, that is part of the appeal: an experiential anchor does not just replace lost footfall, it fills different hours than the store it succeeded.

Mixed-use is the other direction landlords take a stranded anchor box: residential, office, medical, or hotel space woven into what was purely retail, so the center draws a resident and working population that generates its own baseline footfall. The mechanics of using a non-retail tenant as an anchor differ from a straight store lease, which is why mixed-use anchors get their own treatment. Both moves trace back to the same pressure: the department-store anchor decline left large boxes that the market no longer fills the old way.

How landlords prove an anchor is actually pulling traffic

Naming an anchor is easy. Proving it earns its place is where the interesting work is, and it matters commercially: an anchor usually pays little or no base rent precisely because it is supposed to bring the crowd the inline tenants pay premium rent to reach. If the anchor stops pulling, the whole rent structure is built on a claim that is no longer true.

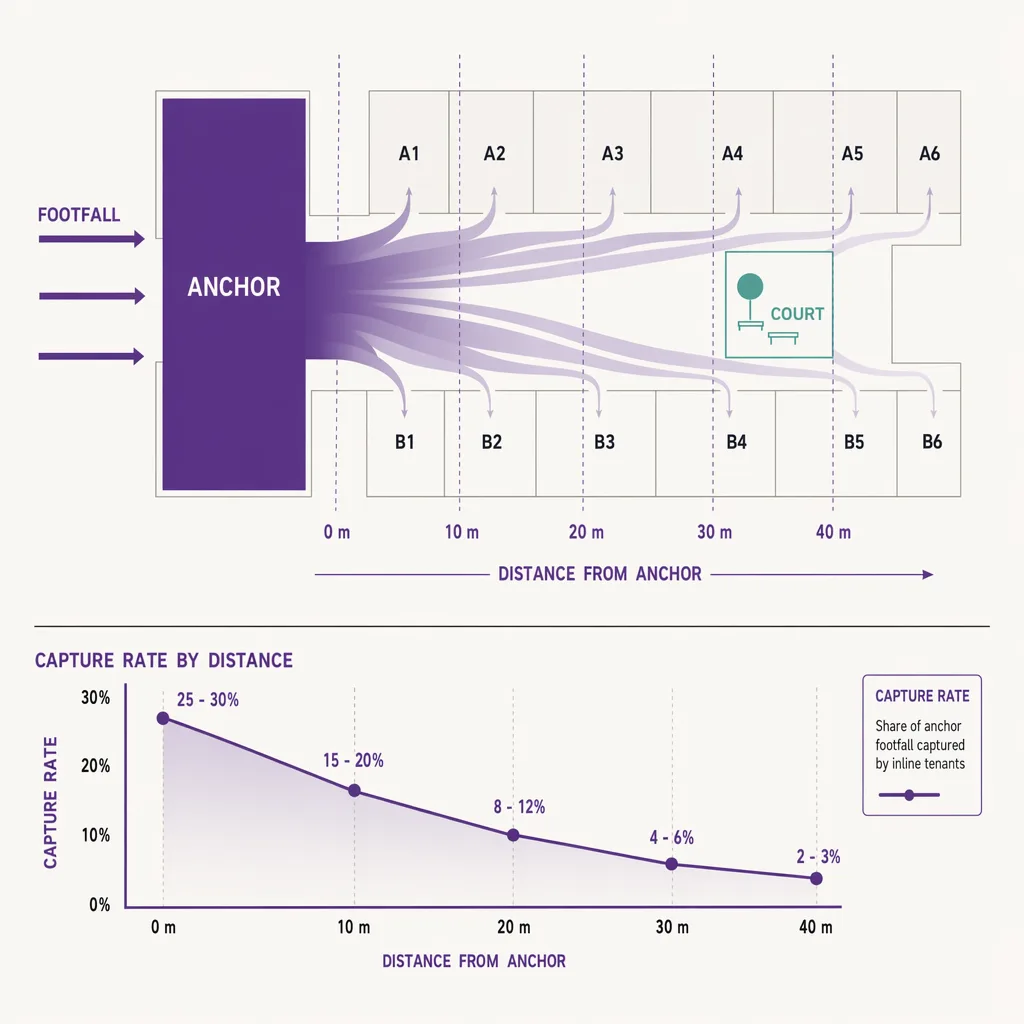

The test is footfall. A landlord who measures entries at the anchor itself, and separately measures the traffic reaching the inline corridors, can see whether the anchor is doing its job or coasting on the center's other draws. The question is not "is the anchor busy" but "how much of the center's traffic exists because of this anchor," and that is answerable only with consistent counts over comparable periods, not with a gut read on how full the store looks.

Ariadne measures this with Hybrid Fusion, its patented camera-free method. Time-of-Flight depth sensing counts every visitor at the entrances, capturing geometry rather than images, while patented phone signal sensing follows movement through the interior, detecting the signals a phone emits even in airplane mode. The sensor streams both feeds to Ariadne, where Hybrid Fusion combines them into one trajectory per visit and computes counts, dwell, and paths. The streams carry no identifier: no MAC address, no device ID, no biometric data, and no camera is involved. Identifiers are stored only when a visitor explicitly opts in, which keeps the method GDPR-friendly and outside biometric territory.

Read against the anchor question, that gives a landlord two numbers that used to be a matter of opinion: how many people the anchor pulls at its own door, and how much of that flow reaches the inline tenants living on it. The second number is the one that settles arguments. An anchor can be busy in isolation and still fail the center if its visitors arrive, shop the anchor, and leave without passing an inline unit, which happens more often than intuition suggests when an anchor sits by its own external entrance. Measuring the spillover, not just the anchor's own count, is what turns "the anchor is doing well" into a claim a landlord can defend at renewal. For the full picture on measuring a center this way, see shopping center analytics.

FAQ

What are the most common examples of anchor tenants?

Department stores and large-format apparel in regional malls, supermarkets and hypermarkets in community and grocery-anchored centers, and warehouse clubs, home-improvement, and other big-box formats in power centers. Increasingly, cinemas, gyms, and food halls anchor space that department stores have vacated.

Is a supermarket an anchor tenant?

Yes. In a community or neighborhood center, a supermarket or hypermarket is the classic anchor. Its draw is frequent and necessity-led, which produces steadier repeat traffic than a discretionary regional mall.

Can a restaurant or food hall be an anchor tenant?

Yes, and it is happening more every year. A food hall or a strong dining cluster sells time spent in the building rather than a product, pulls dedicated evening and weekend visits, and now anchors centers that once relied on retail alone.

Why do department stores no longer anchor malls the way they did?

A wave of full-line closures across 2020 to 2025 left large boxes that landlords rarely refill with another department store. The space tends to be repurposed for experiential, mixed-use, or several smaller high-rent tenants instead.

How does a landlord know if an anchor is really pulling traffic?

By measuring footfall: counting entries at the anchor and, separately, the traffic reaching the inline corridors over comparable periods. That shows whether the anchor is generating the crowd the rest of the center depends on, rather than coasting on other draws.

---