A shopping center runs on a bargain that looks upside down at first glance. The biggest store pays the least. The smallest stores pay the most. The one everyone comes to see hands over almost no rent, while the ones nobody drove specifically to visit carry the building. That inversion is not a mistake. It is the anchor-and-inline relationship, and once you see how the two sides trade with each other, the whole economics of a mall stops looking strange.

This post is a head-to-head. It defines the inline tenant, the term the anchor conversation usually skips, and then runs anchor against inline across the dimensions that actually differ: space, rent, term, traffic dependence, and negotiating leverage. The goal is not to redefine what an anchor is, but to show what sits on the other side of the corridor from it, and why the two need each other in such unequal-looking ways.

What is the difference between an anchor tenant and an inline tenant?

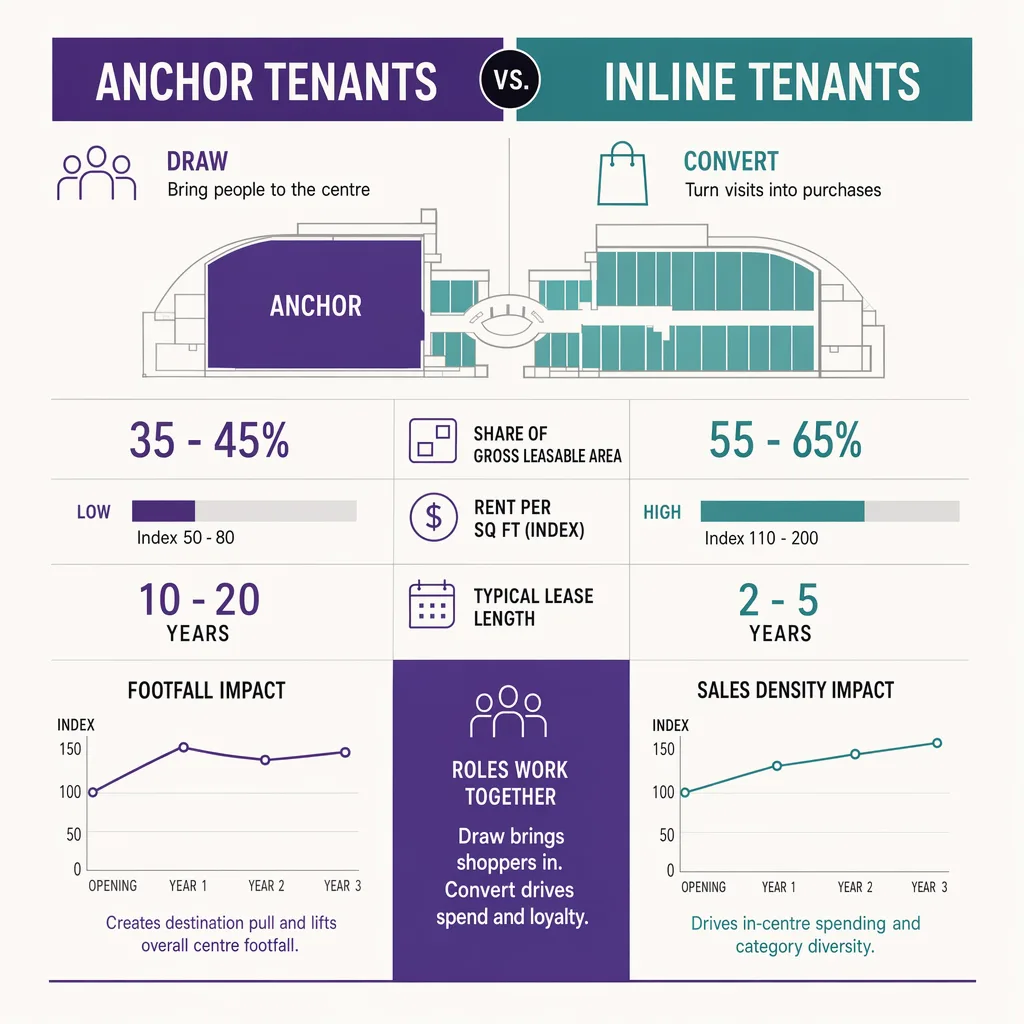

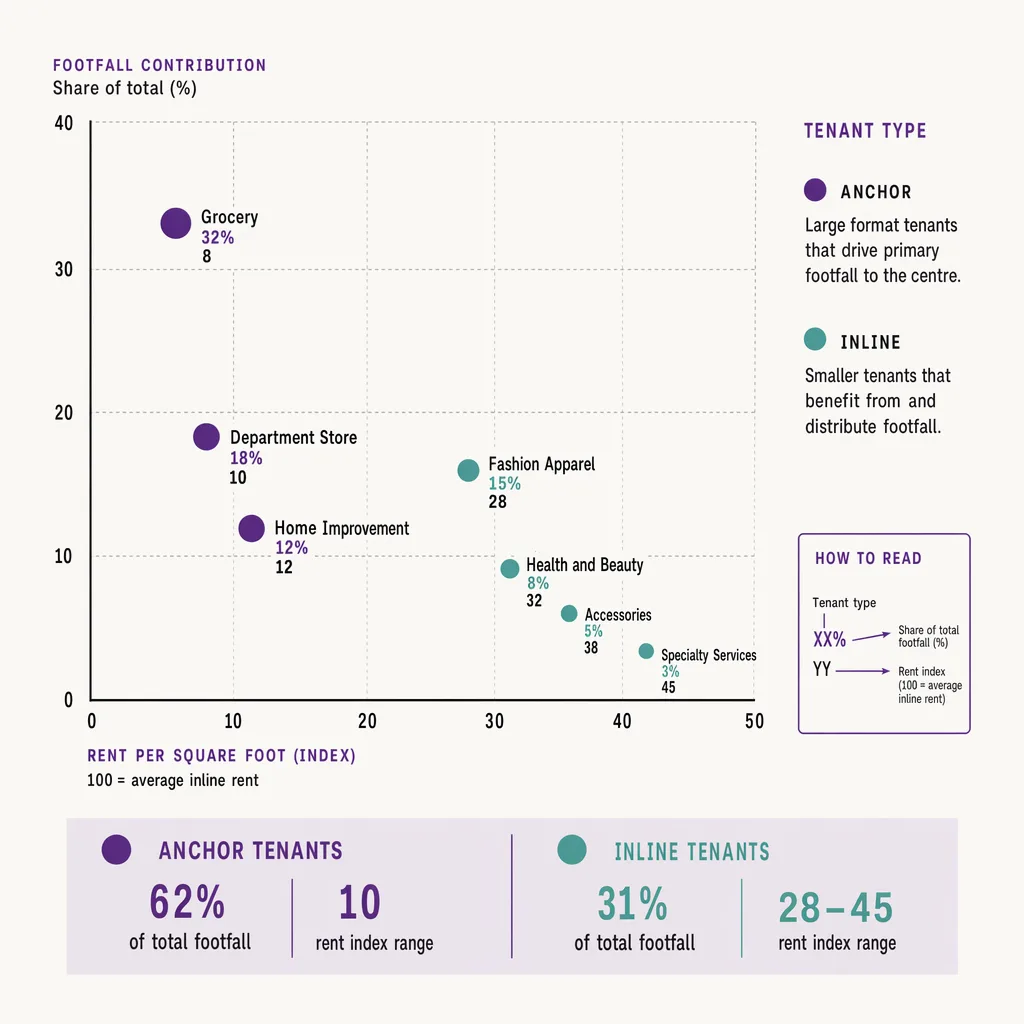

An anchor tenant is the large store that draws the crowd; an inline tenant is one of the smaller shops along the mall corridor that lives on the traffic the anchor pulls. The differences run deep: anchors occupy far more space, pay much lower rent per square foot (sometimes near zero base rent in exchange for the traffic they bring), sign long terms, and hold lease leverage. Inline tenants pay premium rent per square foot, sign shorter terms, and often carry co-tenancy clauses letting them cut rent or leave if the anchor goes dark.

That is the shape of it. The rest of this post fills in each dimension, starting with the side that rarely gets its own definition.

What is an inline tenant?

An inline tenant is a store located in the line of shops along a shopping center's interior corridor, between or around the anchors. The name is literal: these are the units set in a row, in line, facing the walkway that connects one anchor to another. A fashion boutique, a jeweler, a phone accessories kiosk, a bookstore, a shoe shop: the specialty retailers that fill the stretch of mall between the department store at one end and the supermarket or cinema at the other are inline tenants.

The defining trait is not what they sell but where their traffic comes from. An inline tenant does not, on its own, make people get in the car. Very few shoppers set out for the day to visit one specialty store in the middle of a mall. They come for the anchor, or for the mall as a destination, and then they pass the inline stores on the way. The inline tenant's business model is built on capturing a slice of traffic it did not generate. That single fact, dependence on borrowed footfall, drives almost every difference that follows.

Inline tenants are sometimes called specialty tenants or, informally, mall shops. Whatever the label, the structural position is the same: small units, along the corridor, living on the anchor's pull.

It is worth separating inline tenants from two things they are often confused with. A kiosk or cart in the middle of the walkway is not, strictly, an inline unit, since it does not occupy a leased storefront along the line, though it shares the same dependence on passing traffic. And a pad-site or freestanding tenant in the parking field, a bank branch or a drive-through, is not inline either, because it sits outside the corridor and often draws its own visits. The inline tenant is specifically the storefront in the row, and that placement is the whole point: it succeeds or fails on how many of the people walking the corridor between the anchors choose to step inside.

Side by side: the dimensions that differ

Set the two roles against each other and the contrast is sharp on every axis that matters.

- Space (GLA). Anchor tenant: Very large footprint, a department store or supermarket scale unit. Inline tenant: Small footprint, a single corridor unit.

- Rent per square foot. Anchor tenant: Much lower; sometimes near zero base rent in exchange for the traffic it brings. Inline tenant: Premium per square foot, the highest in the center.

- Lease term. Anchor tenant: Long, often measured in decades. Inline tenant: Shorter, measured in years.

- Traffic dependence. Anchor tenant: Generates its own draw; brings the crowd. Inline tenant: Depends on the anchor's and the center's traffic.

- Negotiating leverage. Anchor tenant: High; the landlord needs the anchor to fill the center. Inline tenant: Lower individually; leverage comes from the co-tenancy clause.

Read the table down the two columns and a single story emerges. The anchor gives the center its traffic and is rewarded with cheap space, a long, secure term, and the leverage that comes from being hard to replace. The inline tenant gives the center its rent and accepts premium per-foot pricing, shorter terms, and less individual leverage, in exchange for access to traffic it could never generate alone. Neither side has the better deal in the abstract. They have different deals, matched to what each brings to the building.

One clarification the table forces: rent per square foot is not the same as rent paid. The anchor's low per-foot rate is spread across an enormous footprint, so its total check is not trivial, but on a like-for-like square-foot basis the inline tenant pays far more. That gap is the point of the next section.

Why inline rent subsidizes anchor traffic

The rent inversion is the economic engine of the whole arrangement, and it is worth stating plainly: inline tenants pay a premium partly to fund the discount the anchor receives.

The logic runs in a loop. The landlord needs an anchor to pull traffic, because without a crowd the center is just a row of small shops nobody drives to. To land and keep that anchor, the landlord offers it space at a rate far below what the location would otherwise command, sometimes close to nothing in base rent. That discount is a cost the landlord has to recover somewhere. It gets recovered from the inline tenants, who pay a premium per square foot that reflects the value of the traffic the anchor delivers to their doors.

So the inline tenant is, in effect, paying for two things at once: the physical unit, and a share of the traffic-generation cost that the anchor is not paying itself. The premium is rent for footfall as much as for floor space. This is the heart of how anchor and inline rent compare, and it explains why a landlord fights so hard to keep an anchor filled. An empty anchor does not just leave a large dark box in the building. It removes the traffic that justified every inline tenant's premium rent, which is why the loss of an anchor puts pressure on the entire rent roll, not just one lease.

That interdependence, inline rent funding anchor traffic, funding inline sales, funding inline rent, is the mechanism that holds a traditional mall together. It also explains the clause that protects the weaker side of the bargain.

The same logic is why the anchor holds the negotiating position it does at renewal. The landlord cannot simply raise the anchor's rent to inline levels, because the anchor's cheap rate is not a discount the landlord grants out of generosity, it is the price of the traffic the whole rent roll depends on. Push the anchor too hard and it leaves, and the departure does not cost the landlord one lease, it threatens every inline premium in the building. The anchor knows this, which is why anchors negotiate from strength and inline tenants, individually, do not. An inline tenant's real bargaining power comes not from its own indispensability, which is low, but from the co-tenancy clause that ties its fate to the anchor's presence.

The co-tenancy link: how inline leases protect against anchor loss

If the inline tenant's whole model rests on the anchor's traffic, the obvious question is what happens when the anchor leaves. The answer is written into the inline lease itself, through co-tenancy clauses.

A co-tenancy clause is the inline tenant's insurance against the risk it cannot control. It typically names the anchor, or a threshold of occupancy, and specifies what the inline tenant may do if that condition fails. If the named anchor goes dark, the clause commonly lets the inline tenant switch to a reduced rent, often a percentage of sales instead of the full base rent, or, if the vacancy drags on, terminate the lease and leave.

The clause exists precisely because of the imbalance the table laid out. The inline tenant took on traffic dependence it did not create and cannot fix. Co-tenancy hands it a defined remedy for the one risk that would otherwise sink it through no fault of its own. It also disciplines the landlord: because a dark anchor triggers rent reductions across every inline lease that names it, the landlord has a powerful financial reason to backfill the anchor fast rather than let the box sit empty. In that sense the clause protects the whole center, not only the individual inline store, by aligning the landlord's incentive with the tenants' survival.

Understood this way, the co-tenancy clause is the contractual expression of the same dependence the rent structure creates. The inline tenant pays a premium for the anchor's traffic, and in return demands protection against that traffic disappearing.

What inline tenants can prove with their own door count

For an inline tenant, the anchor relationship is a source of leverage that usually goes unused, because the tenant cannot see its own numbers clearly enough to argue from them. That is a fixable gap.

Consider the situations where an inline tenant is negotiating from a weak position. At renewal, the landlord holds the traffic story and the tenant has only its own sales figures, which conflate how many people passed the door with how well the store converted them. If footfall is soft, the tenant looks like an underperformer when the real problem is the corridor. If footfall is strong and sales are weak, that is a genuine conversion issue the tenant should know about. Without a door count, the tenant cannot tell the two apart, and neither can the landlord.

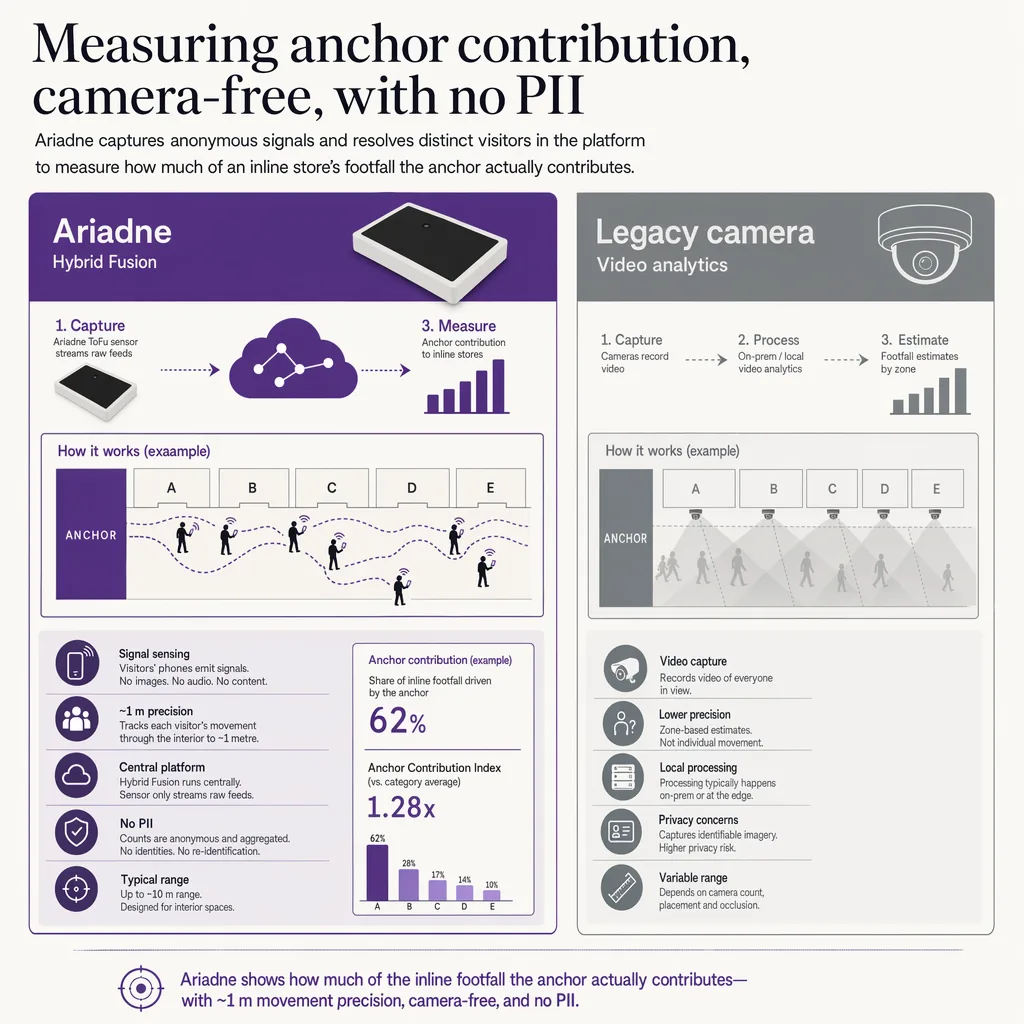

A tenant that measures its own entries can. Counting the people who actually walk through the door, then comparing that against transactions, produces a capture rate: the share of passing corridor traffic the store converts into visits and sales. That single number reframes the negotiation. An inline tenant that can show strong capture on soft corridor traffic has evidence the location is underperforming and grounds to press on rent. One that can show weak capture on strong traffic knows the fix is in the store, not the lease. Reading footfall this way is the foundation of capture rate from corridor traffic, and it turns the inline tenant's structural disadvantage into something it can at least measure and argue from.

Ariadne measures this with Hybrid Fusion, its patented camera-free method. Time-of-Flight depth sensing counts every visitor at the entrances, capturing geometry rather than images, while patented phone signal sensing follows movement through the interior, detecting the signals a phone emits even in airplane mode. The sensor streams both feeds to Ariadne, where Hybrid Fusion combines them into one trajectory per visit and computes counts, dwell, and paths. The streams carry no identifier: no MAC address, no device ID, no biometric data, and no camera is involved. Identifiers are stored only when a visitor explicitly opts in, which keeps the method GDPR-friendly and outside biometric territory.

For an inline tenant, measuring store entries at its own door is the piece of the picture the landlord's center-wide numbers never give it: not how busy the mall was, but how many of those visits reached this specific store. That is the number an inline lease negotiation actually turns on, and it is the one an inline tenant can own outright.

FAQ

What is an inline tenant in a shopping center?

An inline tenant is a store located in the row of shops along a shopping center's interior corridor, between or around the anchors. These are the specialty retailers, boutiques, and kiosks that fill the mall between the larger anchor stores. The defining trait is that they depend on the traffic the anchors and the center draw, rather than generating their own.

What is the difference between an anchor tenant and an inline tenant?

An anchor is the large store that draws the crowd; an inline tenant is a smaller corridor shop that lives on that traffic. Anchors occupy much more space, pay far lower rent per square foot, sign long terms, and hold lease leverage. Inline tenants pay premium rent per square foot, sign shorter terms, and rely on co-tenancy clauses to protect them if the anchor leaves.

Why do inline tenants pay more rent per square foot than anchors?

Because inline rent partly funds the discount the anchor receives. The landlord gives the anchor cheap space in exchange for the traffic it brings, then recovers that cost from inline tenants, who pay a premium reflecting the value of the footfall the anchor delivers to their doors. Inline tenants are paying for traffic as much as for floor space.

What is a specialty tenant?

Specialty tenant is another term for an inline tenant: a smaller retailer along the mall corridor, as opposed to an anchor. The two labels describe the same structural position, small units that depend on the center's traffic rather than generating their own.

How can an inline tenant prove its store is worth the rent?

By measuring its own door count and comparing entries against transactions to calculate a capture rate. That separates how many people passed and entered the store from how well the store converted them, which turns a renewal negotiation from an argument over sales figures alone into one backed by measured corridor traffic and capture performance.